Search within this section

Select a section below and enter your search term, or to search all click Not-for-profit entities

Favorited Content

View image

View image

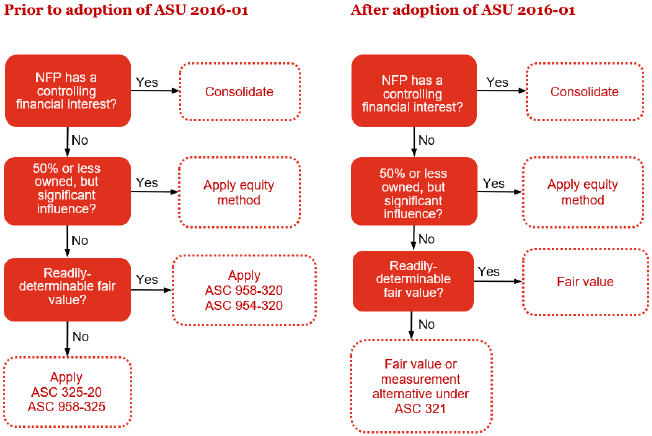

An NFP with a controlling financial interest through direct or indirect ownership of a majority voting interest in a for-profit entity that is other than a limited partnership or similar legal entity shall apply the guidance in the General Subsections of Subtopic 810-10. However, in accordance with paragraph 810-10-15-17, NFPs are not subject to the Variable Interest Entities Subsections of that Subtopic.

For legal entities other than limited partnerships, consolidation is appropriate if a reporting entity has a controlling financial interest in another entity and a specific scope exception does not apply (see Section 810-10-15). The usual condition for a controlling financial interest is ownership of a majority voting interest, but in some circumstances control does not rest with the majority owner.

For legal entities other than limited partnerships, the usual condition for a controlling financial interest is ownership of a majority voting interest and, therefore, as a general rule, ownership by one reporting entity, directly or indirectly, of more than 50 percent of the outstanding voting shares of another entity is a condition pointing toward consolidation. The power to control may also exist with a lesser percentage of ownership, for example, by contract, lease, agreement with other stockholders, or by court decree.

An NFP that owns 50 percent or less of the voting stock in a for-profit entity shall apply the guidance in Subtopic 323-10 unless the investment is measured at fair value in accordance with applicable GAAP, including the guidance described in (e).

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Not-for-profit entities