Search within this section

Select a section below and enter your search term, or to search all click Not-for-profit entities

Favorited Content

View image

View image

View image

View image

NFP model (ASC 958-810)

|

Business entity model (ASC 810-10)

|

|---|---|

|

|

|

|

|

|

|

|

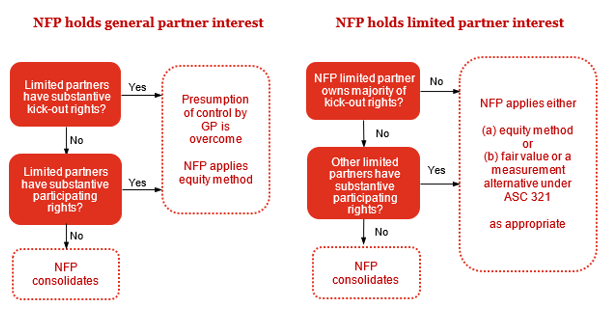

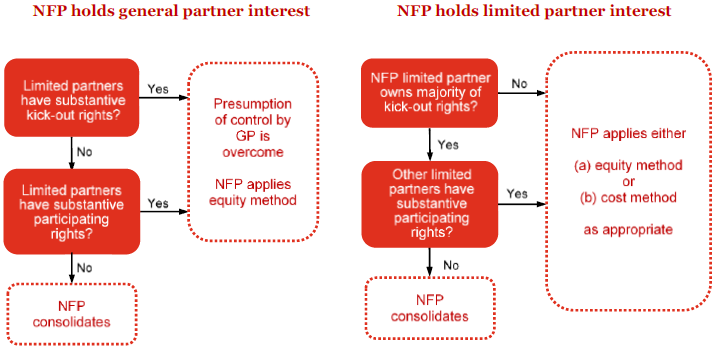

An NFP that is a general partner or a limited partner of a for-profit limited partnership or a similar legal entity (such as a limited liability company that has governing provisions that are the functional equivalent of a limited partnership) shall apply the guidance in paragraphs 958-810-25-11 through 25-29 and 958-810-55-16A through 55-16I. However, the guidance in those paragraphs does not apply to the following:

The general partners in a limited partnership are presumed to control that limited partnership regardless of the extent of the general partners' ownership interest in the limited partnership.

If the limited partners have substantive kick-out rights or substantive participating rights, the presumption of control by the general partners is overcome and each of the general partners shall account for its investment in the limited partnership using the equity method of accounting.

If one limited partner directly or indirectly owns more than 50 percent of a limited partnership’s kick-out rights through voting interests, then that limited partner shall be deemed to have a controlling financial interest in the limited partnership and shall consolidate the limited partnership. However, if noncontrolling limited partners have substantive participating rights, then the limited partner with a majority of kick-out rights through voting interests does not have a controlling financial interest.

Excerpt from ASC 958-810-15-4(d)

An NFP with a more than minor noncontrolling interest in a for-profit real estate partnership, limited liability company, or similar legal entity shall report its noncontrolling interests in such entities using the equity method in accordance with the guidance in Subtopic 970-323 unless that interest is reported at fair value in conformity with the guidance described in [ASC 958-810-15-4](e).

The equity method of accounting for investments in general partnerships is generally appropriate for accounting by limited partners for their investments in limited partnerships. A limited partner's interest may be so minor that the limited partner may have virtually no influence over partnership operating and financial policies. Such a limited partner is, in substance, in the same position with respect to the investment as an investor that owns a minor common stock interest in a corporation, and, accordingly, the limited partner should account for its investment in accordance with Topic 321.

Kick-out rights (voting interest entity definition): The rights underlying the limited partner’s or partners’ ability to dissolve (liquidate) the limited partnership or otherwise remove the general partners without cause.

Participating rights (voting interest entity definition): Participating rights allow the limited partners or noncontrolling shareholders to block or participate in certain significant financial and operating decisions of the limited partnership or corporation that are made in the ordinary course of business. Participating rights do not require the holders of such rights to have the ability to initiate actions.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Not-for-profit entities