Search within this section

Select a section below and enter your search term, or to search all click Property, plant, equipment and other assets

Favorited Content

Definition from ASC Master Glossary

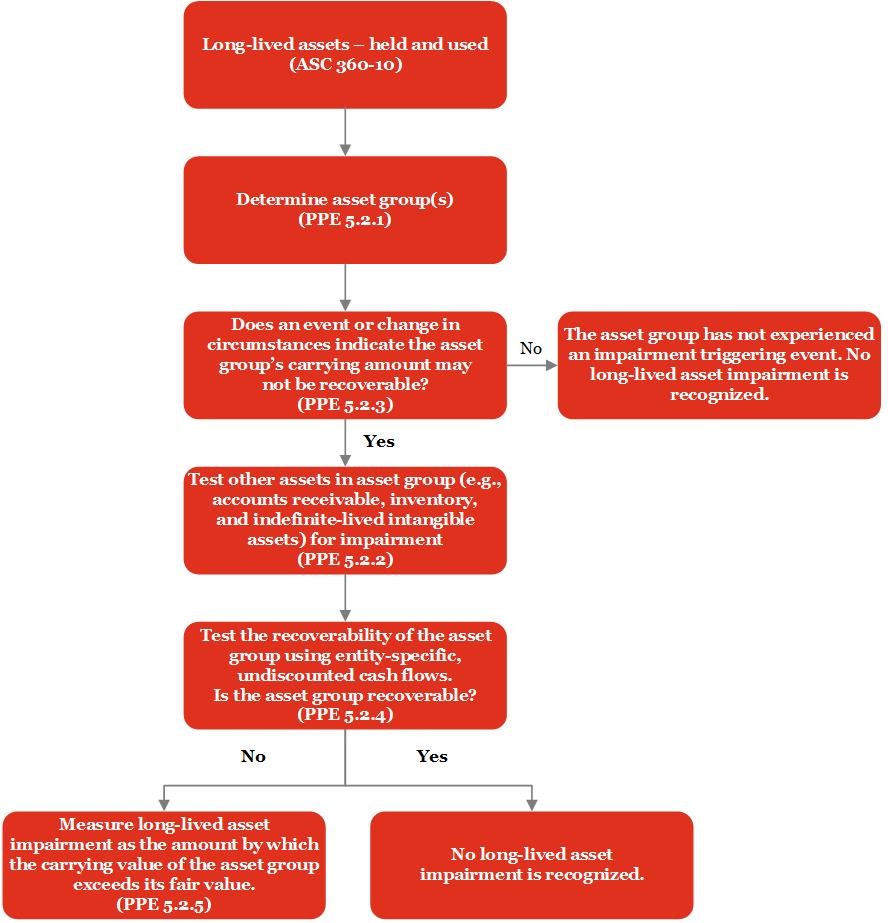

Asset Group: An asset group is the unit of account for a long-lived asset or assets to be held and used, which represents the lowest level for which identifiable cash flows are largely independent of the cash flows of other groups of assets and liabilities.

Excerpt from ASC 360-10-35-21

Excerpt from ASC 360-10-35-31

[T]he primary asset is the principal long-lived tangible asset being depreciated or intangible asset being amortized that is the most significant component asset from which the asset group derives its cash-flow-generating capacity.

Operating cash flows (in millions) |

Cash flows upon sale

|

Total cash flows |

Probability assessment |

Possible cash flows |

|

Two years

|

|||||

No renewal

|

$21

|

$44

|

$65

|

40%

|

$26

|

Renewal

|

$26

|

$44

|

$70

|

60%

|

$42

|

$68

|

|||||

Five years

|

|||||

No renewal

|

$63

|

$13

|

$76

|

50%

|

$38

|

Renewal

|

$71

|

$13

|

$84

|

50%

|

$42

|

Total

|

$80

|

Possible cash flows (in millions) |

Probability assessment |

Probability-weighted cash flows |

|

Two years

|

$68

|

25%

|

$17

|

Five years

|

$80

|

75%

|

$60

|

Total

|

$77

|

Grouping Long-Lived Assets Classified as Held and Used

Allocating Impairment Losses to an Asset Group

Carrying amount |

Fair value |

Difference |

|

PP&E |

$600 |

$100 |

($500) |

Customer relationship |

200 |

300 |

100 |

Patent |

0 |

100 |

100 |

Total |

$800 |

$500 |

($300) |

Carrying amount |

Fair value |

Difference |

|

PP&E |

$600 |

$100 |

($500) |

Customer relationship |

200 |

300 |

100 |

Patent |

0 |

450 |

450 |

Total |

$800 |

$850 |

$50 |

An entity owns a manufacturing facility that together with other assets is tested for recoverability as a group. In addition to long-lived assets (Assets A–D), the asset group includes inventory measured using first-in, first-out (FIFO), which is reported at the lower of cost and net realizable value in accordance with Topic 330, and other current assets and liabilities that are not covered by this Subtopic. The $2.75 million aggregate carrying amount of the asset group is not recoverable and exceeds its fair value by $600,000. In accordance with paragraph 360-10-35-28, the impairment loss of $600,000 would be allocated as shown below to the long-lived assets of the group.

Asset Group |

Carrying Amount (in $000s) |

Pro Rata Allocation Factor |

Allocation of Impairment (Loss) (in $000s) |

Adjusted Carrying Amount (in $000s) |

|||

Current assets |

$400 |

— |

— |

$400 |

|||

Liabilities |

(150) |

— |

— |

(150) |

|||

Long-lived assets: |

|||||||

Asset A |

590 |

24% |

($144) |

446 |

|||

Asset B |

780 |

31 |

(186) |

594 |

|||

Asset C |

950 |

38 |

(228) |

722 |

|||

Asset D |

180 |

7 |

(42) |

138 |

|||

Subtotal — long-lived assets |

2,500 |

100 |

(600) |

1,900 |

|||

Total |

$2,750 |

100% |

($600) |

$2,150 |

If the fair value of an individual long-lived asset of an asset group is determinable without undue cost and effort and exceeds the adjusted carrying amount of that asset after an impairment loss is allocated initially, the excess impairment loss initially allocated to that asset would be reallocated to the other long-lived assets of the group. For example, if the fair value of Asset C is $822,000, the excess impairment loss of $100,000 initially allocated to that asset (based on its adjusted carrying amount of $722,000) would be reallocated as shown below to the other long-lived assets of the group on a pro rata basis using the relative adjusted carrying amounts of those assets.

Long-Lived Assets of Asset Group |

Adjusted Carrying Amount (in $000s) |

Pro Rata Reallocation Factor |

Reallocation of Excess Impairment (Loss)(in $000s) |

Adjusted Carrying Amount after Reallocation (in $000s) |

|||

Asset A |

$446 |

38% |

($38) |

$408 |

|||

Asset B |

594 |

50 |

(50) |

544 |

|||

Asset D |

138 |

12 |

(12) |

126 |

|||

Subtotal |

1,178 |

100% |

(100) |

1,078 |

|||

Asset C |

722 |

100 |

822 |

||||

Total |

$1,900 |

$ - |

$1,900 |

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Property, plant, equipment and other assets